Terry Knowles, European Editor03.24.22

The landscape for the EU’s chemical sector faces several significant and simultaneous changes that are needed to reshape the industry to fulfill the EU’s Green Deal. In short it is required to:

• Become climate neutral.

• Increase circularity.

• Digitalize and implement the Chemical Strategy for Sustainability (CSS).

• Maintain global competitiveness.

The Chemical Strategy for Sustainability alone represents a whole new layer of challenges for the EU chemical industry and CEFIC, the European Chemical Industry Council, has already commissioned and published a report on what the possible consequences are for the industry.

Bearing this in mind, CEFIC asked EU policymakers and EU member state governments to cooperate in converting the CSS into a growth and innovation strategy.

Possible Long-Term Consequence for Industry

Original findings from the first report commissioned by CEFIC showed that something approaching 12,000 substances could fall into the two forthcoming legislative proposals alone, these being changes to Classification, Packaging and Labelling Regulation (CLP) and also the Generic Risk Approach (GRA).

The approximately 12,000 different substances could count for 43% of the European chemical industry’s turnover.

However, attempts to weight the significance of some substances over others in terms of the relative unknowns of definitions and criteria as part of the CSS, it could be that about 28% of the industry’s turnover might be affected. Of this, about a third of the substances might easily be substituted or reformulated.

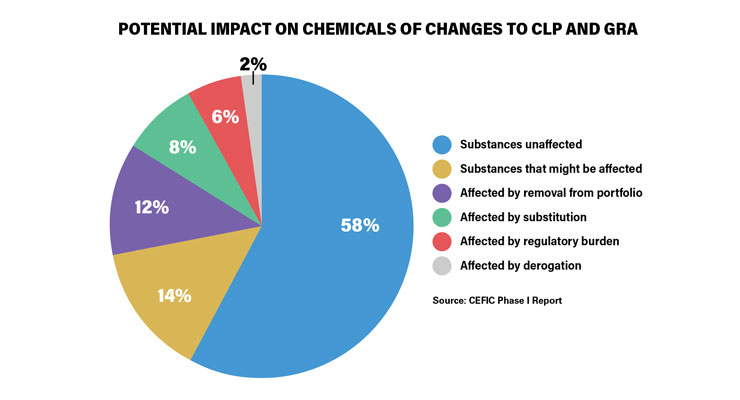

The differing extents of the overall eventualities that may come to pass for the substances is illustrated by the pie chart, which effectively summarizes the quantitative findings of the report. Most concerning is the conclusion that 12% of the collective portfolio (which was based on information from more 100 different major chemical companies in Europe, that generate two-thirds of the collective industry turnover) could end up being removed. This would amount to the industry losing about €70 billion in turnover by 2040.

The qualitative findings of the report are that the impact on downstream users warrants further exploration. The analysis has shown that 74% of products in scope to be impacted by the addition of hazards to CLP and the extension of the GRA are professional or consumer products.

The impacts on these products have been estimated and the results suggest that the downstream user sectors that are most likely to be impacted are generally the formulation industries, particularly (but not limited to) those serving public consumers, such as:

• Polymer preparations and compounds.

• Inks and toners.

• Paints and coatings.

• Washing and cleaning products.

• Adhesives and sealants.

• Cosmetics and personal care products.

• Lubricants and greases.

• Biocidal products and plant protection products.

• Paper and board products.

Recently, leaders from diverse backgrounds joined panels during the EU Industry Days 2022 to outline their expectations of the chemical industry’s Transition Pathway; a co-creation process led by the European Commission aimed at accelerating industry towards the European Green Deal goals. What it appears to amount to is a significant paradigm shift in terms of green technology design for the future.

Europe’s speciality chemicals industry is worth €40 billion and obviously not all companies are industry giants such as Dow, Nouryon, BASF and Neste that were present at the event. Clearly there is a concern for the thousands of SMEs across that depend on the strong regional market.

The Need for a Future Development Framework

Although the challenges laid down by the EU often prompt huge amounts of hard work for chemical companies and industry, leading executives from the aforementioned companies shared something of an appetite for new developments to be prompted in the chemical sector, particularly when the scale of the global chemical production will double or triple over the next 10 years.

In fact, the EU chemicals industry was one of the first to come out in support of the EU Green Deal and has long been advocating the need for a holistic approach to the chemicals industry because of its unique position: chemicals are present in more than 95% of manufactured goods and the EU chemicals industry is a major supplier of all essential and strategic value chains, including pharmaceuticals, electronics, EV batteries, construction materials and more.

The industry’s transition and upcoming policy changes will therefore have a “ripple effect” on many other manufacturing sectors using chemicals (especially those previously listed here).

“The Transition Pathway comes at a very good time,” said Rafael Cayuela, chief strategy officer and corporate chief economist at Dow, referring to the second largest recession Europe has witnessed this century. “The challenges are massive, as is the need for new innovation in the industrial transformation. We don’t have the time, and we don’t have resources or innovation to be wasted,” he said.

“New chemistry takes time. We need to drive innovation and have the right framework to ensure it’s done in a proper way,” said Johan Landfors, president of technology solutions at Nouryon.

Acknowledging the vital role of chemicals to many value chains and enabling products for the transition, he recognized that while alternative chemicals do exist, the right chemistry is needed.

Mercedes Alonso, EVP, renewable polymers and chemicals at Neste, outlined critical factors for the chemicals industry. She called for industry to jointly progress with its entire value chain, to take risks as “we don’t have time to lose” and to stop looking for the silver bullet.”

By way of summing up, Dr. Martin Brudermüller, the CEFIC president and chairman of the board for BASF, said, “The chemical industry thinks in decades rather than years. The simultaneous multiple transitions we are facing make this a ‘make or break’ moment for our sector. For us, it is paramount to have a long-term vision and policy coherence to generate large-scale Green Deal investments between now and 2050.

“Chemicals are key to Europe’s industrial transformation and sustainable competitiveness,” Dr. Brudermüller added. “Europe needs a resilient chemical industry to deliver on the Green Deal. We are looking forward to working with the European Commission and other stakeholders to co-create this dedicated pathway for our industry.”

• Become climate neutral.

• Increase circularity.

• Digitalize and implement the Chemical Strategy for Sustainability (CSS).

• Maintain global competitiveness.

The Chemical Strategy for Sustainability alone represents a whole new layer of challenges for the EU chemical industry and CEFIC, the European Chemical Industry Council, has already commissioned and published a report on what the possible consequences are for the industry.

Bearing this in mind, CEFIC asked EU policymakers and EU member state governments to cooperate in converting the CSS into a growth and innovation strategy.

Possible Long-Term Consequence for Industry

Original findings from the first report commissioned by CEFIC showed that something approaching 12,000 substances could fall into the two forthcoming legislative proposals alone, these being changes to Classification, Packaging and Labelling Regulation (CLP) and also the Generic Risk Approach (GRA).

The approximately 12,000 different substances could count for 43% of the European chemical industry’s turnover.

However, attempts to weight the significance of some substances over others in terms of the relative unknowns of definitions and criteria as part of the CSS, it could be that about 28% of the industry’s turnover might be affected. Of this, about a third of the substances might easily be substituted or reformulated.

The differing extents of the overall eventualities that may come to pass for the substances is illustrated by the pie chart, which effectively summarizes the quantitative findings of the report. Most concerning is the conclusion that 12% of the collective portfolio (which was based on information from more 100 different major chemical companies in Europe, that generate two-thirds of the collective industry turnover) could end up being removed. This would amount to the industry losing about €70 billion in turnover by 2040.

The qualitative findings of the report are that the impact on downstream users warrants further exploration. The analysis has shown that 74% of products in scope to be impacted by the addition of hazards to CLP and the extension of the GRA are professional or consumer products.

The impacts on these products have been estimated and the results suggest that the downstream user sectors that are most likely to be impacted are generally the formulation industries, particularly (but not limited to) those serving public consumers, such as:

• Polymer preparations and compounds.

• Inks and toners.

• Paints and coatings.

• Washing and cleaning products.

• Adhesives and sealants.

• Cosmetics and personal care products.

• Lubricants and greases.

• Biocidal products and plant protection products.

• Paper and board products.

Recently, leaders from diverse backgrounds joined panels during the EU Industry Days 2022 to outline their expectations of the chemical industry’s Transition Pathway; a co-creation process led by the European Commission aimed at accelerating industry towards the European Green Deal goals. What it appears to amount to is a significant paradigm shift in terms of green technology design for the future.

Europe’s speciality chemicals industry is worth €40 billion and obviously not all companies are industry giants such as Dow, Nouryon, BASF and Neste that were present at the event. Clearly there is a concern for the thousands of SMEs across that depend on the strong regional market.

The Need for a Future Development Framework

Although the challenges laid down by the EU often prompt huge amounts of hard work for chemical companies and industry, leading executives from the aforementioned companies shared something of an appetite for new developments to be prompted in the chemical sector, particularly when the scale of the global chemical production will double or triple over the next 10 years.

In fact, the EU chemicals industry was one of the first to come out in support of the EU Green Deal and has long been advocating the need for a holistic approach to the chemicals industry because of its unique position: chemicals are present in more than 95% of manufactured goods and the EU chemicals industry is a major supplier of all essential and strategic value chains, including pharmaceuticals, electronics, EV batteries, construction materials and more.

The industry’s transition and upcoming policy changes will therefore have a “ripple effect” on many other manufacturing sectors using chemicals (especially those previously listed here).

“The Transition Pathway comes at a very good time,” said Rafael Cayuela, chief strategy officer and corporate chief economist at Dow, referring to the second largest recession Europe has witnessed this century. “The challenges are massive, as is the need for new innovation in the industrial transformation. We don’t have the time, and we don’t have resources or innovation to be wasted,” he said.

“New chemistry takes time. We need to drive innovation and have the right framework to ensure it’s done in a proper way,” said Johan Landfors, president of technology solutions at Nouryon.

Acknowledging the vital role of chemicals to many value chains and enabling products for the transition, he recognized that while alternative chemicals do exist, the right chemistry is needed.

Mercedes Alonso, EVP, renewable polymers and chemicals at Neste, outlined critical factors for the chemicals industry. She called for industry to jointly progress with its entire value chain, to take risks as “we don’t have time to lose” and to stop looking for the silver bullet.”

By way of summing up, Dr. Martin Brudermüller, the CEFIC president and chairman of the board for BASF, said, “The chemical industry thinks in decades rather than years. The simultaneous multiple transitions we are facing make this a ‘make or break’ moment for our sector. For us, it is paramount to have a long-term vision and policy coherence to generate large-scale Green Deal investments between now and 2050.

“Chemicals are key to Europe’s industrial transformation and sustainable competitiveness,” Dr. Brudermüller added. “Europe needs a resilient chemical industry to deliver on the Green Deal. We are looking forward to working with the European Commission and other stakeholders to co-create this dedicated pathway for our industry.”