David Savastano, Ink World Editor10.09.09

As 2002 heads into the final quarter, it is clear that the year has not brought the hoped-for gains that were anticipated after the recession in 2001. Rather, as the country grew wary after a number of major corporations collapsed amid what can be best described as questionable accounting practices, the economy has remained sluggish.

The printing industry, in particular, remains slow. In Market Watch on page 16, a recent survey by the Printing Industries of America shows the average printer’s profit to have fallen to 1 percent, the lowest it has been in 30 years. As such, key suppliers to the printing industry, including ink companies, are finding that they are being called upon to further hold or reduce prices.

Ink companies are continuing to do what they can to hold their costs down, by watching their overhead and containing costs wherever possible. They are finding that they have no alternative but to call upon their own suppliers to help share the burden, which is one of the messages that can be found in our “Raw Material Report,” beginning on page 91.

However, there are also other pressures that are being brought to bear on key suppliers to the ink industry. In the middle of August, the price of a barrel of crude oil rose to $29.84. As oil prices increase, the cost of petroleum-based products such as ethylene and polypropylene that can impact the prices of resins, varnishes and additives. Considering the political volatility in key oil-producing regions, the future for crude oil prices remains uncertain.

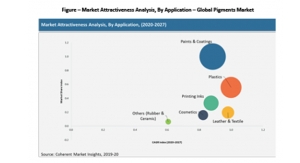

For ink manufacturers, though, the price of pigments remains the most expensive ingredient. Right now, pigments are offering their own challenges.

As imported pigments continue to make gains in the marketplace, pigment prices are remaining low, but there is concern whether suppliers can maintain that level. Ultimately, the possibility exists that key suppliers may look to move away from producing pigments for the ink industry, which would have a significant long-term impact on the market. Interestingly, as the value of the U.S. dollar falls against other currencies, imported pigment producers may begin to feel the economic impact.

On top of these areas, there are other areas that are creating concerns: increased energy prices also adversely affect transportation costs, and other expenses are also accruing, such as increasing costs for meeting environmental standards.

All in all, it has been a difficult 2002 for ink companies, their customers and their suppliers, and only time will tell if a recovery may occur in the coming year.

David Savastano

The printing industry, in particular, remains slow. In Market Watch on page 16, a recent survey by the Printing Industries of America shows the average printer’s profit to have fallen to 1 percent, the lowest it has been in 30 years. As such, key suppliers to the printing industry, including ink companies, are finding that they are being called upon to further hold or reduce prices.

Ink companies are continuing to do what they can to hold their costs down, by watching their overhead and containing costs wherever possible. They are finding that they have no alternative but to call upon their own suppliers to help share the burden, which is one of the messages that can be found in our “Raw Material Report,” beginning on page 91.

However, there are also other pressures that are being brought to bear on key suppliers to the ink industry. In the middle of August, the price of a barrel of crude oil rose to $29.84. As oil prices increase, the cost of petroleum-based products such as ethylene and polypropylene that can impact the prices of resins, varnishes and additives. Considering the political volatility in key oil-producing regions, the future for crude oil prices remains uncertain.

For ink manufacturers, though, the price of pigments remains the most expensive ingredient. Right now, pigments are offering their own challenges.

As imported pigments continue to make gains in the marketplace, pigment prices are remaining low, but there is concern whether suppliers can maintain that level. Ultimately, the possibility exists that key suppliers may look to move away from producing pigments for the ink industry, which would have a significant long-term impact on the market. Interestingly, as the value of the U.S. dollar falls against other currencies, imported pigment producers may begin to feel the economic impact.

On top of these areas, there are other areas that are creating concerns: increased energy prices also adversely affect transportation costs, and other expenses are also accruing, such as increasing costs for meeting environmental standards.

All in all, it has been a difficult 2002 for ink companies, their customers and their suppliers, and only time will tell if a recovery may occur in the coming year.