David Savastano, Editor02.01.21

For consumers and brand owners alike, pigments are the most critical component of inks. They provide the color that catches your eye, which is the signature of a brand. Just think of Tide Orange and Coca-Cola Red.

Ink manufacturers are particularly sensitive when it comes to working with their pigment suppliers. Not only must pigments meet regulatory criteria, but they must also meet production standards.

Jonathan Graunke, VP of UV/EB technology and assistant director of R&D for INX International Ink Co., spoke about the regulatory requirements.

“As we continue to work with the UN Sustainable Development Goals, it’s important we have pigments that meet stringent regulatory thresholds,” said Graunke. “As an example, the certainty that non-intentionally added substances (NIAS) are no longer present is critical. The absence of PAAs, heavy metals, and even pigments designed without halogenated materials such as chlorine, are now high priority areas. Additionally, we need products that will pass recycling protocols, with an emphasis on how they react to recycling washes.

“Of course, we continue to have a need for materials that disperse easier in a multitude of chemistries, improving processing, color development, and finished product characteristics,” Graunke added. “A good example is having yellow pigments that flow better in UV while providing the strengths of traditional diarylides such as yellow 13.”

Lutz Frischmann, global product director flexible packaging for hubergroup, said that one of the most important factors while looking for new pigments is that new sources always need to be in line with ever-changing regulatory demands.

“hubergroup Chemicals is our ‘external’ supplier for pigments because we are aware of their extensive expertise in product safety and regulatory affairs, high delivery capacity and environmental standards,” Frischmann observed. “We have several R&D cooperations. So, we will further continue to rely on the chemicals division’s know-how for the development and source of high-quality pigments.”

“When evaluating new pigments, our list of criteria is extensive and varies depending on the ink chemistry and end-use application,” said Dr. Evan Benbow, VP – product technology and solutions for Wikoff Color.

Anthony Renzi, VP, product management of packaging inks, North American Inks for Sun Chemical, observed that the ink industry, like other chemical related industries, has been greatly influenced by changing consumer trends, environmental regulations, political factors and new technologies.

“These changes have presented both challenges and opportunities for future innovation,” Renzi added. “For existing products, we work closely with our customers to obtain additional registrations where necessary. We are also working closely with our intermediate manufacturers to ensure our pigment supply chain suffers minimal disruption.”

Dr. Benbow said that Wikoff Color considers many factors when sourcing pigments for a given application, including sustainability.

“For example, in packaging ink applications, we require the pigments to meet critical food safety standards, while also being suitable for compostability and recycling applications,” Dr. Benbow added. “These sustainability criteria can include whether the inks become ecotoxic when introduced to compost or whether they stain the de-inking solution or plastics during the recycling process. These factors are important for us to consider as we need pigments that perform for the intended end-use market, but also enable the packaging to stay within the circular economy.”

Frischmann said that sustainability is absolutely an important consideration in sourcing pigments.

“We consider sustainability in all our decisions – no matter what topic it is,” he added. “We follow such as the Cradle to Cradle and the Circular Economy approach. The selection of appropriate color indices is crucial. Our Indian production site, where we produce all our pigments, is well-positioned, and well equipped with a state-of-the-art water recovery plant.”

When it comes to pigments, ink companies are all looking for service, innovation, sustainability and long-standing relationships, among other factors.

Renzi reported that recent rapid moves by Chinese authorities to achieve environmental improvements have greatly impacted many levels of the industry in terms of sustainability.

“With these changes, we’ve seen some cost increases due to a general lack of raw material availability in response to the stronger enforcement of environmental and safety regulations globally,” noted Renzi. “However, sustainability has been a main focus for Sun Chemical in all areas of its business – including sourcing of pigments. These environmental changes are beneficial for all so we will continue moving forward, strengthening partnerships and formulating agility to meet customer and regulation requirements.”

Rick Westrom, INX International Ink Co. SVP of strategic sourcing, said that reliable quality and service and the ability to warehouse locally are essential. “It is very important that each supplier complies with all the global regulatory requirements,” Westrom added.

“In the age of COVID-19, it is imperative for us to work with suppliers that consistently provide Wikoff Color with reliable service and innovative solutions,” said Ken Klug, Wikoff Color’s purchasing director.

“For us, several factors are relevant for the decision, mainly cost and food contact material reasons, but also availability and quality consistency play a role in the decision process,” Frischmann said.

Analysts Discuss the Growing Pigment Market

Analysts say that the pigment market is continuing to grow, although the impact of COVID-19 has been considerable.

For example, Smithers recently offered its insights into the high-performance pigment (HPP) field in its October 2020 report, “The Future of High-performance Pigments to 2025.”

In terms of organic high-performance pigments, Smithers includes benzimidazolones, quinacridones, perylenes, dioxazine violet, isoindolinones and isoindolines, disazo condensations, phthalocyanines, diketo-pyrrolopyrroles and other organic HPPs.

On the inorganic HPP side, Smithers includes complex inorganic colored pigments, bismuth vanadate, ultramarine blue, metal oxides and salts. Smithers adds effect pigments as well.

Smithers research has the global market for high-performance pigments at 243,980 tons in 2019, with a value of $7.07 billion. In 2020 the COVID-19 pandemic and associated disruption to global economic activity affected the market severely.

“Smithers’ latest forecasts show that the market for these pigments fell by 11% in volume to 217,097 tons, while the value dropped by 12% over 2019 to $6.22 billion,“ said John Nelson, editor, Information Division at Smithers. “The market will recover through the first half of the new decade, but is only forecast to reach 255,770 tons and $7.58 billion by 2025.”

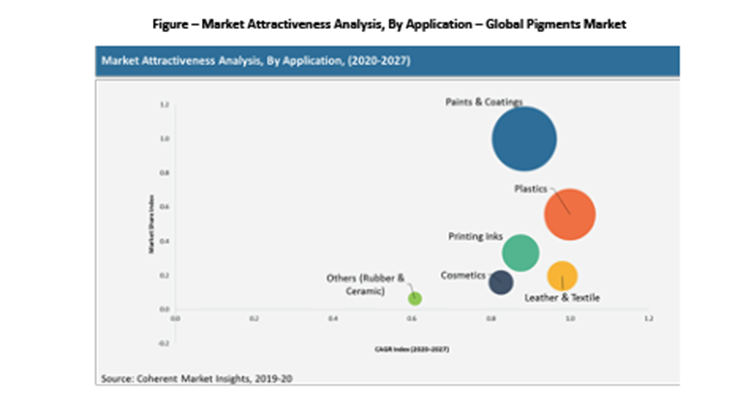

According to “Pigments Market Analysis,” a July 2020 report by Coherent Market Insights (CMI), the global pigments market is estimated to be more than $15 billion in terms of revenue in 2019. CMI sees the market growing at a CAGR of 4.5% during the forecast period (2020-2027). Based on application, paints and coatings dominated the global pigments market in 2019 with approximately 40% of the market share in terms of revenue, followed by printing inks and others.

“The emerging printing inks end-user segment is creating robust demand for pigment and this is projected to serve major market opportunities,” CMI analysts reported. “The growth of the printing inks industry majorly depends on the growth of printing inkjet and laser printing. The rising demand for printing inks from the packaging industry coupled with the growing demand for goods and services around the globe is projected to foster the market growth of pigments.”

According to Coherent Market Insights’ analysis, inorganic pigments had the highest market demand of more than $8.55 billion, accounting for approximately 50% market share in terms of revenue in 2019, followed by organic pigments and specialty (high performance) pigments, accounting for 35% and 15% respectively.

Nelson said that the largest impact through 2020 has been a collapse in demand for products and services that require the use of materials formulated with high-performance pigments.

“Not all segments have been affected to the same extent, and this will continue – even as there are new lockdowns in several countries to cope with a winter surge and new COVID strains,” Nelson added. “Although an initial rebound of 5% recovery in the market for high-performance pigments is forecast for 2021 as some of the most severely impacted end-use applications start to recover, volume demand for these pigments will not reach 2019 levels until 2023/24 at the earliest.”

Smithers reports that decorative paints make up the largest coatings segment for high-performance pigments. Pigments used in printing fell only moderately in 2020; use in printed packaging remained strong, but use in advertising graphics and publications fell more severely.

CMI believes that the increasing price of raw materials used in the manufacturing of the pigments will hamper market growth.

“The primary raw materials used in the production of pigments are carbon-based molecules, natural gas derived mainly from petroleum compounds, benzene, toluene, ethylene, naphthalene and acids,” analysts from Coherent Market Insights reported.

Another major challenge in the pigments industry is the increasing number of regulations on various pigments and their raw materials.

‘For instance, the European Union (EU) has implemented stringent regulations on the use of CMR (carcinogenic, mutagenic, or toxic to reproduction) 1 or 2 graded aromatic amines, lead (Pb) and its compounds, cadmium pigments, aromatic amines graded as CMR category 1 or 2 and their salts, dyes, and pigments. The imposed limitation is due to the adverse impact of amines on human health. Moreover, color additives and pigments which are used in cosmetic products are subjected to a strict system of approval under the US law (Federal Food, Drug, and Cosmetic Act (FD&C Act)),” CMI’s analysts concluded.

There have been concerns about the availability and cost of key pigments and raw materials that help formulate these pigments, such as intermediates.

“China’s dominance of basic chemical production had already brought supply chain disruptions in 2018 and 2019 from the introduction of tighter regulation in that country, a problem exacerbated by trade disputes with the US,” Nelson reported. “The Blue Sky initiative has been strictly enforced from the second half of 2018, with some chemical operations forced to close. These have led to supply chain disruptions and price hikes, which have hit pigment production in China and increased costs.”

The pandemic introduced new challenges to the supply chain, more from transportation issues rather than product availability.

“These were mostly concentrated in Q1 and into Q2 2020, as China entered a strict lockdown, but after this has been able to control virus infections more effectively than major end-use economies in Europe and North America,” Nelson added.

“Many end-users of the chemicals sourced from China were already looking at alternative sources, either from other Asian countries or from domestic production,” Nelson continued. “Through to 2025 new supply chain structures will evolve, as producers of high-value products – including high-performance pigments – will move to localized raw material sourcing. Furthermore, increased competition from Asian pigment producers, and a slowdown in demand for high-performance pigments from key segments – such as automotive – have led to some Western pigment producers reviewing their involvement in this market. This is manifest in recent M&A activity, some of which was delayed temporarily in 2020. As the market recovers and certain key end-use segments remain depressed, further consolidation of the high-performance pigment producers is to be expected.”

CMI noted that China is one of the largest manufacturing bases for pigments and their raw materials. The supply of pigments has been significantly impacted in the last two to three years owing to a shortage of raw materials due to stricter environmental enforcement in China, which has caused various plant closures in the country.

In March 2019, a massive fire explosion occurred at the Jiangsu Tianjiayi Chemical pesticide plant in China and had resulted in nearly 80 deaths. The fire had also spread to various nearby facilities.

The Chinese government had ordered a forced shut-down of factories at the industrial park, which included two key suppliers of 2-methoxy-4-nitro-aniline (PNOA), required for the manufacture of Pigment Yellow 74. These plants were immediately closed, which resulted in an increase in the cost of raw materials, and eventually, an increase in the price of pigments.

Furthermore, the ongoing trade war between the US and China and India and China is also expected to impact the supply and cost of pigment and intermediates in the near future. However, manufacturers are now focusing on various strategies, such as shifting their manufacturing plants from China to other regions/countries such as the Indian Subcontinent, South Korea, or southeast Asian countries, in order to avoid the sanctions imposed on these products.

Abhishek Baheti, a consultant at Coherent Market Insights, believes that such developments will bridge the demand-supply gap and will help in stabilizing the prices of various pigments, their intermediates and raw materials. Moreover, existing players in the pigment industry are focusing on expanding their capacities, in order to meet the increasing demand for pigments.

“As countries emerge from the pandemic, people’s lifestyles and work patterns may evolve differently. This presents opportunities and threats to all markets, including that for high-performance pigments,” said Nelson.

Raj Shah, strategy consultant for Coherent Market Insights, expects the plastic segment to show the fastest growth among other applications, exhibiting a CAGR of 3.5% in terms of revenue, in the forecast period (2020-2027).

“The printing inks segment also accounted for a significant market share, generating revenue of approximately $2.46 billion in terms of value in 2019 and is expected to reach $2.98 billion by 2027, exhibiting a CAGR of 3.1%,” Shah reported. “The growth of the printing inks industry is expected to drive demand for pigments during the forecast period. A further increase in demand for printing inks is expected to lead to higher demand for pigments during the forecast period.”

Brilliant

Superior Daylight Fluorescent Colorants for Printing Ink Applications

Whether you need dry colors for liquid, screen or plastisol inks, soluble toners for high strength flexo applications, or paste concentrates for conventional and UV systems, we have the right product for you!

www.fluorescentcolor.com

Cabot Corporation

Cabot Corporation is a leading manufacturer of carbon black and other specialty chemicals and have long supplied pigments to the inks industry. Our global reach enables us to work closely with customers to meet the highest standards for performance, quality and service. Our global production network and applications development facilities provide our customers with global service capabilities as well as the latest technical innovations.

Our specialty carbon blacks for inks have been formulated to meet application-specific needs and are manufactured to exacting standards.

www.cabotcorp.com

DayGlo Color Corp

Global Leader in Fluorescent Colorants

Cleveland-based DayGlo Color Corp is a global leader in fluorescent colorants, offering a diverse product line and customized color solutions for packaging and consumer goods, plastics, graphic arts, paints and coatings, dyes and textiles, as well as ingredients for the personal care and cosmetics industries. DayGlo’s diverse range of products can be used alone or combined with conventional colors to help achieve cleaner, brighter, more sophisticated colors. With DayGlo, it’s color. Only better.

www.dayglo.com

DCL

Leading Manufacturer of Color Pigments for the Coatings, Plastics and Ink Industries

DCL is a global leader in the supply of color pigments and dispersions for the coatings, plastics and ink industries. And while the name DCL may be new, the people, philosophy, and innovation behind it are anything but. DCL is poised to positively impact our customer’s business by continuing to innovate, rapidly respond to customer needs, and be the difference our customers are looking for. DCL invites the world to “See the Difference We Make.”

www.pigments.com

Ferro Corporation

Discover Our Color Solutions For Your Inks

Ferro Corporation is a leading global supplier of technology-based functional coatings and color solutions. Ferro supplies functional coatings for glass, metal, ceramic and other substrates and color solutions in the form of specialty pigments and colorants for a broad range of industries and applications.

www.ferro.com

HEUBACH

HEUBACH global reliable quality color supplier to the ink industry with more than 600 years of history

HEUBACH supplies the global ink industry with organic HEUCO® pigments and dispersions from the Heubach India plants, and water-based Heucosperse™ and Microsperse™ dispersions for ink made by Heubach LTD. in the US.

www.heubachcolor.com

Meghna Colour Chem

Producers of a Wide Range of Pigments

MCC Pigments is from one of the leading producers of pigments based in India. MCC produces a wide range of pigments for the ink industry ranging from Phthalocyanine Pigments, Activated CPC Blues and Classical Azo pigments. Our huge capacity for producing these pigments and our state-of-the-art manufacturing facility make us a quality and trusted supplier to some of the top ink makers.

www.meghnacolour.com

Schlenk

Effect Pigments: Aluminum, Gold Bronze, Colored Aluminum, Polychromatic

Zenexo WB Series (Gold and Champagne) is automotive OEM grade. It is easily tintable for various color stylings, and offers excellent hide and flop. Zenexo WB is water and solvent compatible, and the powder form is classified as not dangerous.

www.schlenk.com

The Shepherd Color Company

The Shepherd Color Company, a Global Producer of Complex Inorganic Color Pigments

The Shepherd Color Company is a global producer of Complex Inorganic Color Pigments (CICPs) used in a variety of industries and applications where performance is critical under the most extreme conditions. Our main products, Arctic® Infrared Reflective Pigments, Dynamix® Easy Dispersible Pigments, and StarLight® Special Effect Pigments are supplied to customers around the world. Our pigments are highly engineered ceramic colorants, meaning they are more durable, more consistent, and more functional.

www.shepherdcolor.com

TRUST CHEM

TRUST CHEM IS THE BIGGEST PRODUCER AND EXPORTER OF ORGANIC PIGMENTS FROM CHINA

Trust Chem is the fourth largest manufacturer and supplier of organic pigments in the world, with headquarters located in Hangzhou, China. Subsidiaries in Europe, North America, Australia, India and South Africa make Trust Chem a true global supplier to the color industry. In Trust Chem’s four manufacturing plants in Asia, we produce a wide range of pigment technologies, including Phthalocyanie, Classical Azo, HPP Azo, Benzimidazolone, Disazo Condensation, Anthraquinone, Isoindolinone, Isoindoline and Quinacridone pigments.

www.trustchemusa.com

Ink manufacturers are particularly sensitive when it comes to working with their pigment suppliers. Not only must pigments meet regulatory criteria, but they must also meet production standards.

Jonathan Graunke, VP of UV/EB technology and assistant director of R&D for INX International Ink Co., spoke about the regulatory requirements.

“As we continue to work with the UN Sustainable Development Goals, it’s important we have pigments that meet stringent regulatory thresholds,” said Graunke. “As an example, the certainty that non-intentionally added substances (NIAS) are no longer present is critical. The absence of PAAs, heavy metals, and even pigments designed without halogenated materials such as chlorine, are now high priority areas. Additionally, we need products that will pass recycling protocols, with an emphasis on how they react to recycling washes.

“Of course, we continue to have a need for materials that disperse easier in a multitude of chemistries, improving processing, color development, and finished product characteristics,” Graunke added. “A good example is having yellow pigments that flow better in UV while providing the strengths of traditional diarylides such as yellow 13.”

Lutz Frischmann, global product director flexible packaging for hubergroup, said that one of the most important factors while looking for new pigments is that new sources always need to be in line with ever-changing regulatory demands.

“hubergroup Chemicals is our ‘external’ supplier for pigments because we are aware of their extensive expertise in product safety and regulatory affairs, high delivery capacity and environmental standards,” Frischmann observed. “We have several R&D cooperations. So, we will further continue to rely on the chemicals division’s know-how for the development and source of high-quality pigments.”

“When evaluating new pigments, our list of criteria is extensive and varies depending on the ink chemistry and end-use application,” said Dr. Evan Benbow, VP – product technology and solutions for Wikoff Color.

Anthony Renzi, VP, product management of packaging inks, North American Inks for Sun Chemical, observed that the ink industry, like other chemical related industries, has been greatly influenced by changing consumer trends, environmental regulations, political factors and new technologies.

“These changes have presented both challenges and opportunities for future innovation,” Renzi added. “For existing products, we work closely with our customers to obtain additional registrations where necessary. We are also working closely with our intermediate manufacturers to ensure our pigment supply chain suffers minimal disruption.”

Dr. Benbow said that Wikoff Color considers many factors when sourcing pigments for a given application, including sustainability.

“For example, in packaging ink applications, we require the pigments to meet critical food safety standards, while also being suitable for compostability and recycling applications,” Dr. Benbow added. “These sustainability criteria can include whether the inks become ecotoxic when introduced to compost or whether they stain the de-inking solution or plastics during the recycling process. These factors are important for us to consider as we need pigments that perform for the intended end-use market, but also enable the packaging to stay within the circular economy.”

Frischmann said that sustainability is absolutely an important consideration in sourcing pigments.

“We consider sustainability in all our decisions – no matter what topic it is,” he added. “We follow such as the Cradle to Cradle and the Circular Economy approach. The selection of appropriate color indices is crucial. Our Indian production site, where we produce all our pigments, is well-positioned, and well equipped with a state-of-the-art water recovery plant.”

When it comes to pigments, ink companies are all looking for service, innovation, sustainability and long-standing relationships, among other factors.

Renzi reported that recent rapid moves by Chinese authorities to achieve environmental improvements have greatly impacted many levels of the industry in terms of sustainability.

“With these changes, we’ve seen some cost increases due to a general lack of raw material availability in response to the stronger enforcement of environmental and safety regulations globally,” noted Renzi. “However, sustainability has been a main focus for Sun Chemical in all areas of its business – including sourcing of pigments. These environmental changes are beneficial for all so we will continue moving forward, strengthening partnerships and formulating agility to meet customer and regulation requirements.”

Rick Westrom, INX International Ink Co. SVP of strategic sourcing, said that reliable quality and service and the ability to warehouse locally are essential. “It is very important that each supplier complies with all the global regulatory requirements,” Westrom added.

“In the age of COVID-19, it is imperative for us to work with suppliers that consistently provide Wikoff Color with reliable service and innovative solutions,” said Ken Klug, Wikoff Color’s purchasing director.

“For us, several factors are relevant for the decision, mainly cost and food contact material reasons, but also availability and quality consistency play a role in the decision process,” Frischmann said.

Analysts Discuss the Growing Pigment Market

Analysts say that the pigment market is continuing to grow, although the impact of COVID-19 has been considerable.

For example, Smithers recently offered its insights into the high-performance pigment (HPP) field in its October 2020 report, “The Future of High-performance Pigments to 2025.”

In terms of organic high-performance pigments, Smithers includes benzimidazolones, quinacridones, perylenes, dioxazine violet, isoindolinones and isoindolines, disazo condensations, phthalocyanines, diketo-pyrrolopyrroles and other organic HPPs.

On the inorganic HPP side, Smithers includes complex inorganic colored pigments, bismuth vanadate, ultramarine blue, metal oxides and salts. Smithers adds effect pigments as well.

Smithers research has the global market for high-performance pigments at 243,980 tons in 2019, with a value of $7.07 billion. In 2020 the COVID-19 pandemic and associated disruption to global economic activity affected the market severely.

“Smithers’ latest forecasts show that the market for these pigments fell by 11% in volume to 217,097 tons, while the value dropped by 12% over 2019 to $6.22 billion,“ said John Nelson, editor, Information Division at Smithers. “The market will recover through the first half of the new decade, but is only forecast to reach 255,770 tons and $7.58 billion by 2025.”

According to “Pigments Market Analysis,” a July 2020 report by Coherent Market Insights (CMI), the global pigments market is estimated to be more than $15 billion in terms of revenue in 2019. CMI sees the market growing at a CAGR of 4.5% during the forecast period (2020-2027). Based on application, paints and coatings dominated the global pigments market in 2019 with approximately 40% of the market share in terms of revenue, followed by printing inks and others.

“The emerging printing inks end-user segment is creating robust demand for pigment and this is projected to serve major market opportunities,” CMI analysts reported. “The growth of the printing inks industry majorly depends on the growth of printing inkjet and laser printing. The rising demand for printing inks from the packaging industry coupled with the growing demand for goods and services around the globe is projected to foster the market growth of pigments.”

According to Coherent Market Insights’ analysis, inorganic pigments had the highest market demand of more than $8.55 billion, accounting for approximately 50% market share in terms of revenue in 2019, followed by organic pigments and specialty (high performance) pigments, accounting for 35% and 15% respectively.

Nelson said that the largest impact through 2020 has been a collapse in demand for products and services that require the use of materials formulated with high-performance pigments.

“Not all segments have been affected to the same extent, and this will continue – even as there are new lockdowns in several countries to cope with a winter surge and new COVID strains,” Nelson added. “Although an initial rebound of 5% recovery in the market for high-performance pigments is forecast for 2021 as some of the most severely impacted end-use applications start to recover, volume demand for these pigments will not reach 2019 levels until 2023/24 at the earliest.”

Smithers reports that decorative paints make up the largest coatings segment for high-performance pigments. Pigments used in printing fell only moderately in 2020; use in printed packaging remained strong, but use in advertising graphics and publications fell more severely.

CMI believes that the increasing price of raw materials used in the manufacturing of the pigments will hamper market growth.

“The primary raw materials used in the production of pigments are carbon-based molecules, natural gas derived mainly from petroleum compounds, benzene, toluene, ethylene, naphthalene and acids,” analysts from Coherent Market Insights reported.

Another major challenge in the pigments industry is the increasing number of regulations on various pigments and their raw materials.

‘For instance, the European Union (EU) has implemented stringent regulations on the use of CMR (carcinogenic, mutagenic, or toxic to reproduction) 1 or 2 graded aromatic amines, lead (Pb) and its compounds, cadmium pigments, aromatic amines graded as CMR category 1 or 2 and their salts, dyes, and pigments. The imposed limitation is due to the adverse impact of amines on human health. Moreover, color additives and pigments which are used in cosmetic products are subjected to a strict system of approval under the US law (Federal Food, Drug, and Cosmetic Act (FD&C Act)),” CMI’s analysts concluded.

There have been concerns about the availability and cost of key pigments and raw materials that help formulate these pigments, such as intermediates.

“China’s dominance of basic chemical production had already brought supply chain disruptions in 2018 and 2019 from the introduction of tighter regulation in that country, a problem exacerbated by trade disputes with the US,” Nelson reported. “The Blue Sky initiative has been strictly enforced from the second half of 2018, with some chemical operations forced to close. These have led to supply chain disruptions and price hikes, which have hit pigment production in China and increased costs.”

The pandemic introduced new challenges to the supply chain, more from transportation issues rather than product availability.

“These were mostly concentrated in Q1 and into Q2 2020, as China entered a strict lockdown, but after this has been able to control virus infections more effectively than major end-use economies in Europe and North America,” Nelson added.

“Many end-users of the chemicals sourced from China were already looking at alternative sources, either from other Asian countries or from domestic production,” Nelson continued. “Through to 2025 new supply chain structures will evolve, as producers of high-value products – including high-performance pigments – will move to localized raw material sourcing. Furthermore, increased competition from Asian pigment producers, and a slowdown in demand for high-performance pigments from key segments – such as automotive – have led to some Western pigment producers reviewing their involvement in this market. This is manifest in recent M&A activity, some of which was delayed temporarily in 2020. As the market recovers and certain key end-use segments remain depressed, further consolidation of the high-performance pigment producers is to be expected.”

CMI noted that China is one of the largest manufacturing bases for pigments and their raw materials. The supply of pigments has been significantly impacted in the last two to three years owing to a shortage of raw materials due to stricter environmental enforcement in China, which has caused various plant closures in the country.

In March 2019, a massive fire explosion occurred at the Jiangsu Tianjiayi Chemical pesticide plant in China and had resulted in nearly 80 deaths. The fire had also spread to various nearby facilities.

The Chinese government had ordered a forced shut-down of factories at the industrial park, which included two key suppliers of 2-methoxy-4-nitro-aniline (PNOA), required for the manufacture of Pigment Yellow 74. These plants were immediately closed, which resulted in an increase in the cost of raw materials, and eventually, an increase in the price of pigments.

Furthermore, the ongoing trade war between the US and China and India and China is also expected to impact the supply and cost of pigment and intermediates in the near future. However, manufacturers are now focusing on various strategies, such as shifting their manufacturing plants from China to other regions/countries such as the Indian Subcontinent, South Korea, or southeast Asian countries, in order to avoid the sanctions imposed on these products.

Abhishek Baheti, a consultant at Coherent Market Insights, believes that such developments will bridge the demand-supply gap and will help in stabilizing the prices of various pigments, their intermediates and raw materials. Moreover, existing players in the pigment industry are focusing on expanding their capacities, in order to meet the increasing demand for pigments.

“As countries emerge from the pandemic, people’s lifestyles and work patterns may evolve differently. This presents opportunities and threats to all markets, including that for high-performance pigments,” said Nelson.

Raj Shah, strategy consultant for Coherent Market Insights, expects the plastic segment to show the fastest growth among other applications, exhibiting a CAGR of 3.5% in terms of revenue, in the forecast period (2020-2027).

“The printing inks segment also accounted for a significant market share, generating revenue of approximately $2.46 billion in terms of value in 2019 and is expected to reach $2.98 billion by 2027, exhibiting a CAGR of 3.1%,” Shah reported. “The growth of the printing inks industry is expected to drive demand for pigments during the forecast period. A further increase in demand for printing inks is expected to lead to higher demand for pigments during the forecast period.”

Brilliant

Superior Daylight Fluorescent Colorants for Printing Ink Applications

Whether you need dry colors for liquid, screen or plastisol inks, soluble toners for high strength flexo applications, or paste concentrates for conventional and UV systems, we have the right product for you!

www.fluorescentcolor.com

Cabot Corporation

Cabot Corporation is a leading manufacturer of carbon black and other specialty chemicals and have long supplied pigments to the inks industry. Our global reach enables us to work closely with customers to meet the highest standards for performance, quality and service. Our global production network and applications development facilities provide our customers with global service capabilities as well as the latest technical innovations.

Our specialty carbon blacks for inks have been formulated to meet application-specific needs and are manufactured to exacting standards.

www.cabotcorp.com

DayGlo Color Corp

Global Leader in Fluorescent Colorants

Cleveland-based DayGlo Color Corp is a global leader in fluorescent colorants, offering a diverse product line and customized color solutions for packaging and consumer goods, plastics, graphic arts, paints and coatings, dyes and textiles, as well as ingredients for the personal care and cosmetics industries. DayGlo’s diverse range of products can be used alone or combined with conventional colors to help achieve cleaner, brighter, more sophisticated colors. With DayGlo, it’s color. Only better.

www.dayglo.com

DCL

Leading Manufacturer of Color Pigments for the Coatings, Plastics and Ink Industries

DCL is a global leader in the supply of color pigments and dispersions for the coatings, plastics and ink industries. And while the name DCL may be new, the people, philosophy, and innovation behind it are anything but. DCL is poised to positively impact our customer’s business by continuing to innovate, rapidly respond to customer needs, and be the difference our customers are looking for. DCL invites the world to “See the Difference We Make.”

www.pigments.com

Ferro Corporation

Discover Our Color Solutions For Your Inks

Ferro Corporation is a leading global supplier of technology-based functional coatings and color solutions. Ferro supplies functional coatings for glass, metal, ceramic and other substrates and color solutions in the form of specialty pigments and colorants for a broad range of industries and applications.

www.ferro.com

HEUBACH

HEUBACH global reliable quality color supplier to the ink industry with more than 600 years of history

HEUBACH supplies the global ink industry with organic HEUCO® pigments and dispersions from the Heubach India plants, and water-based Heucosperse™ and Microsperse™ dispersions for ink made by Heubach LTD. in the US.

www.heubachcolor.com

Meghna Colour Chem

Producers of a Wide Range of Pigments

MCC Pigments is from one of the leading producers of pigments based in India. MCC produces a wide range of pigments for the ink industry ranging from Phthalocyanine Pigments, Activated CPC Blues and Classical Azo pigments. Our huge capacity for producing these pigments and our state-of-the-art manufacturing facility make us a quality and trusted supplier to some of the top ink makers.

www.meghnacolour.com

Schlenk

Effect Pigments: Aluminum, Gold Bronze, Colored Aluminum, Polychromatic

Zenexo WB Series (Gold and Champagne) is automotive OEM grade. It is easily tintable for various color stylings, and offers excellent hide and flop. Zenexo WB is water and solvent compatible, and the powder form is classified as not dangerous.

www.schlenk.com

The Shepherd Color Company

The Shepherd Color Company, a Global Producer of Complex Inorganic Color Pigments

The Shepherd Color Company is a global producer of Complex Inorganic Color Pigments (CICPs) used in a variety of industries and applications where performance is critical under the most extreme conditions. Our main products, Arctic® Infrared Reflective Pigments, Dynamix® Easy Dispersible Pigments, and StarLight® Special Effect Pigments are supplied to customers around the world. Our pigments are highly engineered ceramic colorants, meaning they are more durable, more consistent, and more functional.

www.shepherdcolor.com

TRUST CHEM

TRUST CHEM IS THE BIGGEST PRODUCER AND EXPORTER OF ORGANIC PIGMENTS FROM CHINA

Trust Chem is the fourth largest manufacturer and supplier of organic pigments in the world, with headquarters located in Hangzhou, China. Subsidiaries in Europe, North America, Australia, India and South Africa make Trust Chem a true global supplier to the color industry. In Trust Chem’s four manufacturing plants in Asia, we produce a wide range of pigment technologies, including Phthalocyanie, Classical Azo, HPP Azo, Benzimidazolone, Disazo Condensation, Anthraquinone, Isoindolinone, Isoindoline and Quinacridone pigments.

www.trustchemusa.com